Why Buy Stock?

A Share of Stock represents a portion of ownership in a corporation. Common stock is one of the riskiest investments because losses of 50% or more are common.

Our government, our corporations, Wall Street and its lackeys, including AAII, have been relentlessly promoting mass stock ownership for the last thirty or so years.

In 1978, Congress amended the Internal Revenue Code by adding section 401(k), whereby employees are not immediately taxed on deferred compensation.

The law went into effect on January 1, 1980, and by 1983 almost half of large firms were offering 401(k) plans.

In 1998, Congress passed legislation that allowed employers to automatically deduct money from employee paychecks for these plans.

By 2006, there were seventy-million participants from OVER 400,000 companies with more than $3 trillion of assets. http://en.wikipedia.org/wiki/401(k)

That means that in 2006, the average participant had about $43,000 and the average baby boomer had about $80,000 in a 401(k) plan.

Interesting numbers.

The primary reason for the explosion of these plans is that they cost employers absolutely nothing because the employer can pass all the costs, and more importantly, all the risks on to the participants.

The problem, of course, is that very few people made money on stocks over the last ten years, and absolutely no one knows if the 10% stock market returns that have been relentlessly promoted will ever be seen again.

Our leaders and the masters of Wall Street are probably Praising the Lord, that we are not France.

IF we were France, then here's one likely ending.

Can the Stock Market be beaten?

For every investor that outperforms the market by one dollar, there MUST be an investor that underperforms the market by the same amount.

That means there are gonna be winners, and it means there are gonna be losers.

After transaction costs are factored into the equation, it means there are gonna be more losers than winners.

Most studies show that about 80% of all professional investors UNDER-PERFORM appropriate indices after transaction costs are considered.

Since 80% of all professional investors underperform appropriate indices, 80% of this presentation will be used to explain the major challenges confronting them in their quest to beat the market. The remaining 20% of this presentation will be used to explain how and why the market may be beaten, and why some amateur investors may have an advantage over the professionals.

Why does anyone buy individual stocks?

There is only one logical reason for buying individual stocks:

Individual stocks are bought to outperform the market.

One common method of selecting individual stocks

My broker recommended the stock.

This is probably the most bizarre reason to buy stock because brokers are paid to churn portfolios. Furthermore, brokers frequently recommend stocks to their clients because they have been given an additional financial incentive to tout the stock.

A second common method of selecting individual stocks

The "boy" who shined my shoes recommended the stock to me.

Believe it or not, many New York City residents believe that shoeshine "boys" working Wall Street are privy to insider information when they overhear conversations.

If you're looking for hot stock tips, the shoeshine "boy" OR a newspaper story OR your favorite "Money Honey" are all probably at least as reliable as your broker.

There are an infinite number of ways amateur investors select stocks.

Some of them may even work over the short run.

And a short run of luck is all you really need. Luck is a very important factor in life.

How do institutional investors select stocks?

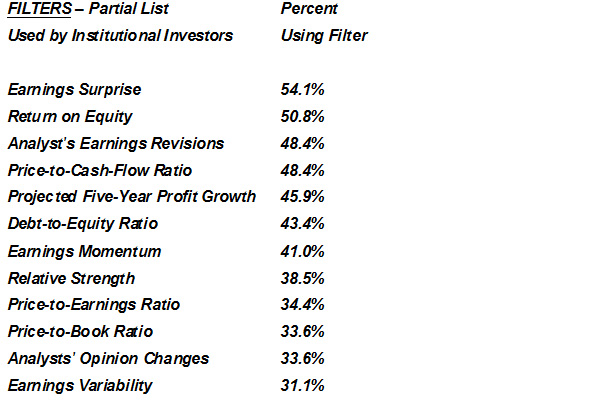

A Stock Screen is a tool investors can use to filter stocks.

Most Stock Screens use multiple filters to select stocks.

There are probably an infinite number of filters.

First I'll show you a partial list that was published in Barrons about ten years ago.

This is a partial list showing the filters that are used most frequently. The first column shows the filter and the second column shows the percentage of institutional investors using the filter.

Key Statistics on Yahoo Finance

Valuation Measures

Financial

Highlights

Management Effectiveness

Income Statement

Balance Sheet

Trading Information

Share Statistics

Dividends & Splits

Many Key Statistics on all these topics for any listed stock are available on Yahoo Finance.

Most of these filters and Key Statistics, and many others are being used by almost all professional and reasonably serious amateur investors in an attempt to outperform the market.

I'm going to talk about one of them because I believe it's worth saying a few words about this filter. Most of the others are important too, but I'm not willing to spend the time required to describe them at this point

According to Barrons, an Earnings Surprise Filter is the filter that is used most frequently by institutional investors.

What's an Earnings Surprise?

There are thousands of professional stock analysts in the United States and there are millions of amateur stock analysts. Most of them focus on earnings, because it is earnings that drive the market. Earnings are the main reason stock markets increase or decrease from one year to the next.

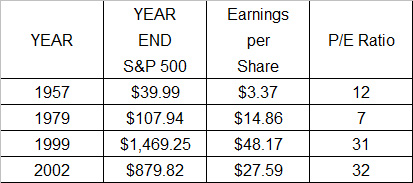

For example, the Standard and Poor's 500 Index is an index that consists of 500 large companies that are actively traded in the United States. This index represents about 75% of the value of the US stock market, and is probably the best proxy for the US economy.

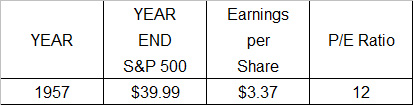

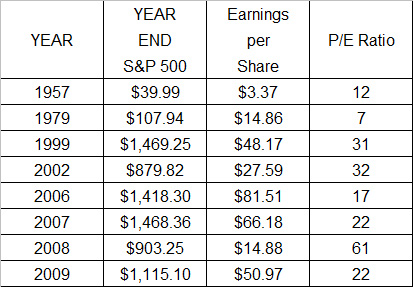

The Index was created in 1957

At the end of 1957, the Index had a value of $40.33 and it earned

$3.42

Its Price Earnings Ratio, or Price divided by Earnings at that time was 12

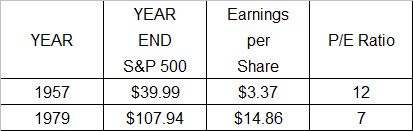

The minimum PE Ratio since 1957 was 7 in 1979

Many investors believe a low PE Ratio is an indicator of an

undervalued stock or an undervalued market.

That may be true, but if you wait for the single digit PE ratios of

1979 to manifest themselves again, you are probably going to have a

long, long wait.

It took the Index twenty-two years to get from $40.33 to $105.76.

That's a return of 4.5% per year excluding dividends.

Dividends added about 3.7% per year during those years.

1979 was the dawn of the greatest bull market the United States has

ever seen.

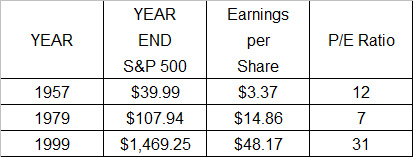

It took the Index twenty years to get from $107.94 to $1,469.25

That's a return of 14.1% per year excluding dividends.

Dividends added about 3.3% per year during those years.

At the end of 1999, the S&P 500 had a value of $1,469.25

That was the S&P 500's highest yearly closing value thru 1999.

Now that we all have the wonderful benefit of hindsight, most of us know that the S&P 500 did not have a yearly close at a higher value until 2013, when it closed at $1,848.36

After 1999 a three year slide down began. A three year slide down had not been seen in the US since the depression of the thirties. Note that both the index and its earnings fell a total of about 40% during this three year slide.

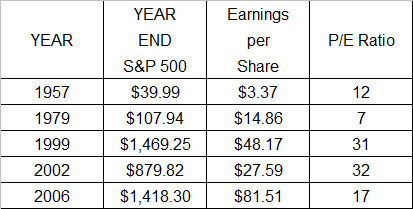

At the end of 2006, the Index had a value of $1,418.30 and it earned $81.51

Earnings that high had never been reported.

Note that if the mood had been as exuberant as it was during the roaring nineties, then earnings of $81.51 suggest an index value of almost $2,500

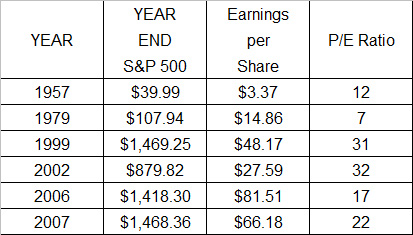

At the end of 2007, the index rose, but earnings fell. On the one hand, an analyst could explain this as a temporary earning's glitch; on the other hand, it could be explained as the forerunner of a coming collapse.

Now that we all have the wonderful benefit of hindsight, we all know that the earning's fall of 2007 signaled the collapse of 2008

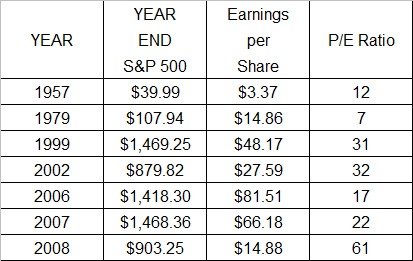

At the end of 2008, the S&P 500 had a value of $903.25 and it earned $14.88

Earnings that low had not been reported since the seventies, and suggest a more appropriate index value of less than $500

A PE Ratio of 61 had never been reported.

Now that we all have the wonderful benefit of hindsight again, we know that Year End 2008 was one of the best buying opportunities of the decade, even though the index had the highest recorded PE Ratio in history.

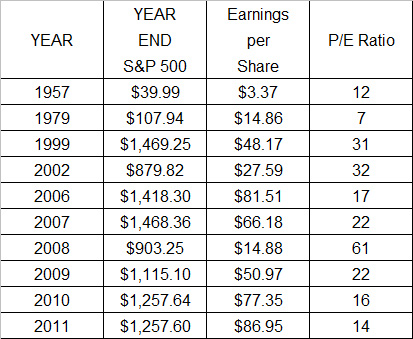

At the end of 2011, the S&P 500 had a value of $1,257.60 and its earnings were $86.95

The relationship between the price of an index and its earnings is loose, but two things are certain:

Lower earnings are bad, and will generally drive the price down.

Higher earnings are good, and will generally drive the price up.

What's an Earnings Surprise?

An earnings surprise is an earnings announcement that was totally unanticipated by the professional analysts that monitor the stock or the index.

A positive surprise will generally drive the price up. And a negative surprise will generally drive the price down.

Is that a rational response?

It would be a rational response if future earnings could be predicted. A stream of steadily increasing historical earnings is frequently used to buy a stock or a stock market. An unanticipated increase in earnings could be a good reason to buy the stock or its market, if there were good reasons to believe the earnings increases would continue.

So, the BIG question is: Can future earnings be predicted?

ALL the evidence indicates that future earnings can NOT be predicted.

During the sixties various and sundry academicians and corporations in the United States and Great Britain conducted studies to determine earning's growth rates.

The studies showed that earning's growth in one period is only 6% correlated to growth in a prior period.

That means that projecting future earning's growth rates from historical growth is a useless exercise.

So the next BIG question is: Why do 54% of institutional investors pay any attention to Earnings Surprises, since it is reasonably well known that earnings are essentially 94% random?

Because, for irrational reasons that are not completely understood, over a short run, a stock's price, and a stock market's price will generally rise after a positive earnings surprise and vice versa.

If you enjoy playing irrational games, then you will probably enjoy playing the stock market game, and you will probably enjoy playing the game of life.

AAII has about 60 different stock screens that use some of the filters that were shown.

ALL stock screens have been successful at some time in the past. Some stock screens will probably be successful in the future.

But ALL stock screens will NOT be successful in the future.

If you are a beginner, then the stock screen you choose is almost certain to fail shortly after you begin using it.

Some beginners may get lucky, but beginners are never competent. That's why they're called beginners.

The masters of Wall Street love beginners because they are a great source of income.

Most folks know that before anyone gets good at anything, a steep learning curve MUST be climbed. If you don't recognize that fact, then chances are pretty good that you're gonna be a beginner forever.

Is it possible to predict anything?

Our lives are dependent on our ability to successfully predict future events, but the record is not good if the known and unknown variables are constantly changing.

Here are some examples:

We are going to bring Peace & Democracy to Iraq and Afghanistan

Mission Accomplished

DOW 30,000

You can't go wrong with Real Estate

Change you can Believe in

Most folks know that the future is uncertain when the future is dependent on known and unknown variables.

But that did NOT prevent the "experts" from making ridiculous predictions.

And it did NOT prevent many of us from believing things that we now know were complete nonsense.

Regardless of all that, the BIG question is:

Can stock screens be used to identify outperforming stocks before the fact?

Most of the remainder of this presentation will attempt to answer that question, but before we get started, let's talk about the weather, because comparing weather forecasters to stock market forecasters may give you a comprehensive understanding of the challenges facing the forecasters.

We are all familiar with weather forecasts. Some of us may even know how accurate they are. If you don't know, then you will know in a few minutes.

A Brief History of Weather Forecasting

Weather forecasting has existed for thousands of years. For much of human existence, weather forecasting was believed to be the province of the gods.

Astrologers were among the first weather forecasting professionals, predicting the weather − along with war, plague, pestilence, and other major events.

Almanacs contained the first published weather forecasts, dating back as far as 3,000 B.C. in ancient Egypt, and have remained popular ever since.

During 1995 the National Weather Service had a budget of about $2 billion to operate an extensive network of weather stations, satellites, balloons, radar ships, and buoys.

How accurate are the short term forecasts i.e., what's it gonna be like tomorrow?

It depends on the forecast.

There are essentially TWO types of forecasts. It is EXTREMELY important to have a comprehensive understanding of the difference between them.

1. The Naive Forecast

2. The Skillful Forecast

Example of a naive weather forecast:

Question: What will tomorrow's weather be like?

Answer:

The same as today's

As a matter of fact, meteorologists use two types of naive forecasts to gage forecasting skill:

1. Persistence − The prediction that tomorrow's weather will be the same as today's.

2. Climatology − The prediction that tomorrow's weather will be the same as seasonal averages.

In fact, persistence and climatology forecasts are right most of the time. That's why you don't have to be too bright to be a "pretty good" weather forecaster.

Meteorologists define skill as a measure of improvement over persistence and climatology.

So, the BIG question is:

Exactly how much value does a skillful meteorologist add to the random guesses of a naive weather forecaster?

Before 1988, the answer was, "Not much value at all."

So, of course, Congress gave the National Weather Service $4 billion to upgrade.

Now the National Weather Service can forecast general weather conditions within a twelve hour period with considerable skill, but wild deviations from weather forecasts can and do occur when atmospheric conditions are chaotic.

If conditions are chaotic, then lead times rapidly diminish

Tornadoes are generally predicted with about 10 MINUTES of lead time, but only 64% of the warnings result in tornadoes.

Severe thunderstorms are generally predicted with 18 MINUTES of lead time.

Flash floods are generally predicted with 21 MINUTES of lead time, but 58% of flash floods were complete surprises. No lead time was given.

Here are the bottom lines:

The data show that the National Weather Service is indeed able to make two or three day predictions with a reasonable degree of accuracy UNLESS chaotic events occur.

The data also show that it is not easy for a skillful weather forecaster to add value to the forecast of a naive forecaster.

Next I'm going to talk about economic forecasts, but before I do, I'm going to emphasize that in theory, the weather, especially over the short term, should be fairly easy to predict because it's a SIMPLE closed loop system and it follows natural laws that were discovered a few hundred years ago.

It is also important to recognize that the weather follows seasonal patterns that can be predicted by almost anyone with reasonable accuracy.

However, a weather system is a chaotic system that is TOTALLY determined by non-linear laws. Non-linear laws are laws that amplify the smallest errors in the initial conditions of the system, making the system unpredictable beyond short periods.

A stock or the economy on which the stock is dependent is NOT a SIMPLE closed loop system, meaning the events that are likely to have the greatest impact have not yet been recognized or perhaps even discovered.

AND, it may follow seasonal patterns, but unlike the weather, it is not required to follow seasonal patterns.

A single stock or an economy is called a complex system rather than a chaotic system.

Complex systems have no natural laws governing their behavior.

Complex systems cannot be dissected into their component parts.

IMPORTANT: Complex systems exhibit periods of order and predictability, punctuated by unexpected moments of self-generated turmoil.

Complex systems adapt to their environments and evolve, exhibiting new behaviors that can invalidate previously established theories.

Complex systems have no fixed cycles; their histories do not repeat themselves.

Modern "Free Market" economies AND their underlying stocks are complex systems that follow a boom-bust business cycle whose amplitude and frequency cannot be predicted.

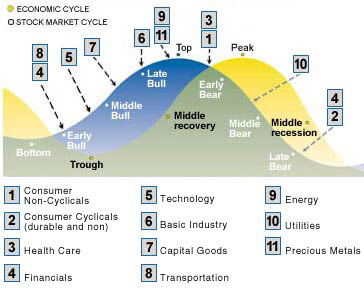

This chart shows a deceptively simple economic cycle and a deceptively simple stock market cycle.

There is no doubt that the economy experiences booms and busts, and there is no doubt that the stock market generally attempts to anticipate the economic cycle. Sometimes the stock market anticipates a boom or a bust correctly, but there is very little evidence to suggest the stock market anticipates the booms or busts with greater accuracy than would be achieved with random guesses.

Look at the economic cycle. Where are we now?

Are we still in a trough or are we in the middle of a recovery?

Perhaps we have already peaked out; perhaps the next step is a double dip recession?

It is tempting to believe someone knows the answers to these questions, but all the evidence shows that the best economists money can buy, cannot answer these questions more accurately than the folks standing on street corners, who claim they're willing to work for food.

During the 1920s Nikolai Kondratieff, a Soviet economist, published a series of reports hypothesizing that capitalist economies experience long term cycles of boom and bust every fifty-four years.

Stalin liked the idea of capitalist economies going bust, but a prediction of recovery earned Kondratieff a one-way ticket to Siberia.

However, normally you're pretty safe if you make long term forecasts. It will take a long time to prove you were wrong, and chances are pretty good that no one will remember your forecast if it was wrong.

There are about 150,000 registered economists

in the United States. Almost all of them are employed by the

economic forecasting industry.

This is a presentation about stocks and the screens that are used to forecast their performance, but stock performance is almost entirely determined by the underlying economy. So, once again, how good are the forecasts?

At any given point in time there are thousands of forecasts available. Some of them are gonna be wrong and some of them are gonna be right.

The First Law of Economics: For every economist, there is an equal and opposite economist.

Here are the bottom lines:

Economists cannot predict the turning points in the economy.

Economists' forecasting skills are about as good as guessing that next year will be the same as last year i.e., the naive forecast.

The naive forecast is a better predictor than economists' forecasts for highly volatile statistics, such as interest rates.

There are no economic forecasters who consistently lead the pack in forecasting accuracy. The leaders in one quarter are likely to be the losers in the next quarter.

How to succeed as an economic forecaster:

Forecast often

and don't keep records.

John Kenneth Galbraith said this a long time ago:

The only function of economic forecasting is to make astrology look

respectable.

So far I have shown that the weather is a chaotic system that can be predicted about 24 hours in advance by simply making a naive forecast i.e., tomorrow's weather will be the same as today's unless a chaotic event interferes.

I have also shown that modern economies and their underlying stocks are complex systems that cannot be forecasted as accurately as the weather with any degree of certainty.

In spite of the fact that the behavior of economies and stocks cannot be predicted, a huge number of folks make a good living selling the future. Most of them work on a real or virtual Wall Street.

There are two

Holy Grails of investing

Timing the Market and Stock Selection.

There are two Schools of Stock Selection

Technical Analysis and Fundamental Analysis

Technical analysts look at charts consisting of historical data because they believe the future performance of a stock or a stock market can be predicted by examining the patterns of the past.

Sometimes these naive forecasts seem to work, but most stock market analysts believe technical analysts are the clowns of Wall Street.

Usually technical analysts are very good at explaining what happened yesterday. William Eng wrote a book called The Technical Analysis of Stocks, Options and Futures

Here is Eng's after the fact explanation for the October 1987 stock market crash:

"The planet of constriction and want, Saturn, is in the tenth house, the house of fame and reputation. For the whole month of October 1987, the planet of good fortune, Jupiter, is transiting the tenth house, first forward, then backward, finally continuing forward again in November. All that was needed was a trigger to set off the chain reaction of ultimate contraction".

So, now you know exactly why the market crashed in October 1987.

I was surprised to learn technical analysts frequently consult astrologers to make their predictions. In fact, Douglas Martin of The New York Times interviewed a Wall Street astrologer who claimed to have 15,000 Wall Street clients seeking astrological books, software, and consulting advice.

The idea that stock prices are random was first developed by French mathematician Louis Bachelier in 1900.

His work was later dubbed the Random Walk Theory based on a 1905 article in Nature magazine on how to predict the location of a drunk walking through a field.

In the 1960s, Arnold Moore and Eugene Fama statistically analyzed stock prices over the periods 1951 thru 1962, and found that stock prices had a 3% correlation from one day to the next.

That means that past stock prices are useless in predicting future stock prices.

Predicting the future remains an elusive goal, especially when one relies on astrology and technical analysis, but the masters of Wall Street are being paid about $100 billion annually to continue the quest.

Fundamental Stock Analysis

Many who consider themselves serious investors reject technical analysis for all the reasons I mentioned, and turn to the Fundamental Analysis of Stocks because fundamentalists believe they are selecting stocks scientifically.

Fundamental Stock Analysis

Step 1. Estimate the intrinsic value of the stock.

Estimating the intrinsic value of a stock involves determining the future earnings discounted at a rate reflecting the riskiness of the stock.

Intrinsic Value = Future Earnings divided by Discount Rate

Two variables:

1. Future earnings

2. Discount rate determined by perceived risk

Sounds easy, doesn't it?

Benjamin Graham, Warren Buffet's mentor, is the father of fundamental analysis. He developed this system after he lost almost everything speculating before the depression.

However, thanks to all the work done by various and sundry academicians and corporate analysts, we all know something Ben did NOT know:

The barriers to predicting the future value of a stock or its market begin with the "Future Earnings" part of the equation. I mentioned it before, but I'll mention it again because it's important.

ALL the evidence indicates that future earnings can NOT be predicted.

During the sixties various and sundry academicians and corporations in the United States and Great Britain conducted studies to determine earnings growth rates.

ALL the studies showed that earnings growth in one period is only 6% correlated to growth in a prior period. That means that projecting future earnings growth rates from historical growth is a useless exercise.

Can perceived risk be determined?

If earnings cannot be predicted, and if you believe that the price of a stock or its market is in large part determined by future earnings, then it follows that risk cannot be determined.

Intrinsic Value = Future Earnings divided by Discount Rate

Two variables:

1. Future earnings are unknowable.

2. Discount rate determined by perceived risk is unknown.

Intrinsic Value = The UNKNOWABLE divided by The UNKNOWN

If Market Technicians are the Clowns of Wall Street, then Fundamentalists must be the Jokers.

In spite of the fact that Future Earnings cannot be determined with any reasonable assurance, in spite of the fact that the Discount Rate cannot be determined with any accuracy and in spite of the fact that these facts are reasonably well known, Benjamin Graham's classic book, Security Analysis, which was written in 1934, is still being peddled today.

What the peddlers of his book don't tell you, is that in 1976, at the end of his life, Ben offered this:

"One lucky break may count for more than a lifetime of effort." He was referring to 1948, when he put $720,000, which was 25% of his portfolio, into GEICO. By 1975 the value received from that investment had passed half a billion dollars! That's an annualized return of more than 27%.

Once again, luck is a very important factor in life.

Recommendations

There are about five thousand publicly listed companies in the United States. One of the important functions of the $100 billion a year financial services industry is to determine the intrinsic value or the fair market value of stocks. Thousands of professional analysts spend their lives attempting to gain an advantage over the competition.

Every major corporation has scores of executives, thousands of employees, and hundreds of investment bankers, lawyers, accountants, consultants and other advisers, many with access to proprietary information. It would be naive to believe that these insiders resist the opportunity to make money on their privileged information, if by no other means than by passing the information along.

Recommendation 1

Before you buy a stock, ask yourself this: What do I know about this

stock that thousands of professional analysts and scores of insiders

do NOT know?

If you cannot convince yourself that you know more than ALL of them, then you are what Business Week calls a turkey i.e., an outsider playing an insider's game.

Every investor has an infinite number of choices, but one of the most important questions to ask yourself is this:

Should I buy an Index Fund or should I buy individual stocks?

Recommendation 2

If you decide to buy individual stocks or even actively managed

stock funds, then benchmark your performance against an APPROPRIATE

index.

What's an appropriate index?

Investors frequently compare their performance to the Dow Jones Industrial Average or the S&P 500 or the NASDAQ 100 because these are well known indices.

2010 Returns including Dividends and other Distributions

14.91% Vanguard S&P 500 Index Fund (Ticker VFINX)

20% Your Portfolio

You can proudly tell anyone willing to listen that you're a genius because you beat the market, but the question intelligent investors ask themselves is this:

Did I beat an APPROPRIATE index?

The answer to that question depends on the contents of your portfolio. The S&P 500 is a capitalization weighted index, so if you held a representative sample consisting of a minimum of 25 stocks, and if you beat the S&P 500, then you could pat yourself on the back, and say, "Well done".

Why is it necessary to hold a minimum 25 stock representative sample?

It is extremely difficult to determine if outperformance is attributable to the luck of a naive beginner, the skill of an expert, or the luck of an expert. Most statisticians agree that holding fewer than 25 stocks would make it impossible to make a determination.

That's the reason it's essentially impossible to gauge the performance of an actively managed DOW portfolio: Hold 25 stocks and it will almost guarantee that you duplicate the performance of the 30 stock DOW; hold much fewer than 25 and it's impossible to determine if you're lucky or skillful.

However, what if your portfolio consisted of small cap stocks? Would it be appropriate to compare your portfolio to large cap indices?

Why or why not?

2010 Returns including Dividends and other Distributions

14.91% Vanguard S&P 500 Index Fund (Ticker VFINX)

27.72%

Vanguard Small Cap Index Fund (Ticker NAESX)

20% Your Small Cap

Portfolio

As you can see, the Vanguard Small Cap Index Fund outperformed your small cap portfolio by considerable margins.

If you were a professional portfolio manager, then there is a very good reason to compare your portfolio to whatever index you are outperforming because a large part of professional portfolio management is conducted with smoke and mirrors.

However, if you were managing your own portfolio, then here's what you did:

You presumably spent a great deal of time and effort creating an intelligent Small Cap portfolio. Not only did you waste your time and effort, but you wasted a great deal of money.

Congratulations.

That's why it's important to compare your performance to an APPROPRIATE index, and that's why it's important not to bet too much of your portfolio on an attempt to beat the market.

The One Handed Economist

Harry Truman said this a long time ago: "All my economists say, on the one hand or the other. − Give me a one-handed economist."

I'm not an economist, but I can tell you there are NO successful one-handed economists.

The One

Handed Economist does NOT survive

It is important to remember that if you cannot make a compelling

argument for one hand OR the other, then you probably do NOT

understand the problem.

That is almost always true in economics, and it is frequently

true in life.

The difficult problems seldom have simple solutions.

This presentation is about 80% complete. So far I have given you the results of studies that show economic forecasts are wrong about as often as they are right, and I have shown that technical or fundamental analyses of stocks add no value to a naive random selection of stocks.

Since I am not one handed, the remaining 20% of this presentation will be dedicated to my other hand. That is, I will argue that the market can be beaten.

I will confine my arguments to the stock selection arena because this presentation is about stock selection, and because I have NOT been able to add significant value by timing the market.

Earlier I said that modern economies and businesses are complex systems that exhibit periods of order and predictability, punctuated by unexpected moments of self-generated turmoil.

Most investors rely on the periods of order and predictability.

If these periods did not outnumber the moments of turmoil, then capitalism could not, and would not survive.

Some investors are even able to anticipate the moments of turmoil and profit from them. However, remember that Tornadoes are generally predicted with about 10 MINUTES of lead time, but only 64% of the warnings result in tornadoes.

That means that if you listen to all the Chicken Littles in the world, you would probably NEVER buy stock.

Regardless, most studies show that about 20% of active portfolio managers beat appropriate indices in any given year.

A 20% chance of success is not a bad chance.

Most high stakes games have far fewer winners.

Most business experts believe that a new business startup has a 1/3 chance of eventually turning a profit, a 1/3 chance of breaking even, and a 1/3 chance of never leaving a negative earnings scenario.

Those facts may explain why the stock market game has an enduring attraction. If you play the stock market game, then you will probably hear about many methods to beat the market. Some of them may even work.

My newsletter partner, Doug Weimer, and I are momentum investors. During the nine years ending December 31, 2010, our stock selections have returned a total of 813.0% versus 29.5% for the S&P 500

That's an annualized return of 27.9% for us and 2.9% for the S&P 500

A more appropriate index for us is a small or micro cap index, but we beat them by almost the same margins.

That either means we are very lucky OR it means we know something about stock selection.

Once again, it is NOT easy to determine whether a stock picker is good or simply lucky.

Some statisticians claim it would take seventy years of performance history to make an accurate determination.

It's pretty safe to say that no one will EVER be able to determine if Doug and I are good, or simply lucky.

So, how did we do it?

Most of you have probably heard of the Efficient Market Hypothesis. It essentially states that the market knows everything there is to know about a stock, so there is no way to outsmart the market.

What does the market really know?

There are about five thousand stocks listed on US exchanges. Thousands of professional analysts are investing trillions of dollars, mostly in the largest 1,000 companies, called the Fortune 1,000 or the Russell 1,000.

It has been estimated that 99% of everything that affects a stock's price is known by the analysts and insiders of the Fortune 1,000. Scores of professional analysts also monitor the next 2,000 largest companies in the US, sometimes referred to as the Russell 2,000.

Hypothesis of the Market's Knowledge

The Largest 1,000 US Companies are 99% Known

The next Largest 2,000 US Companies are 60% to 99% Known

These 3,000 companies represent about 98% of the stock market value in the US.

Hypothesis of the Market's Knowledge

98% of Stock Market Value

The Largest 3,000 US Companies are 60% to 99% Known

2% of Stock Market Value

The Smallest 2,000 US Companies are 5% to 60% Known

Weimer and Wirth restrict ourselves to the smallest 2,000 companies in the United States because our data show these are generally the most profitable and, more importantly, professional investors cannot trade in this arena because it is too illiquid.

It is generally hypothesized that this is probably the only arena in which amateurs have a reasonable chance of beating the professionals.

How do we find these tiny companies?

Every quarter all listed companies are required to report their earnings. I download data on all the companies that have reported improved earnings.

That means that every quarter I download the earnings, revenues, historical prices and key statistics on about two thousand stocks.

The historical prices are downloaded three times: Once after the earnings are announced, next after ten trading days have elapsed so I can determine the market's immediate response to key data, and finally three and a half months after the earnings have been announced so I can determine their long term performance.

Three months is long term performance in the stock market game.

Earnings are reported every three months. That means everything could change in a three month period, and it frequently does.

How much time does it take to process data?

Downloading data usually takes me an average of about ten hours a week. But it takes a lot more than ten hours to analyze and optimize the data.

The bottom line is that during a five week earning's season it takes me about forty or fifty hours a week to process data.

If I wished, I could easily spend much more time playing the game, and sometimes I do.

The bottom line is that this is a highly competitive game because there is no shortage of talented amateurs in this world. If Doug and I did not make continuous improvements to our stock selection criteria, then we would quickly be left behind.

Earlier I mentioned that during the nine years ending December 31, 2010, our stock selections returned a total of 813.0% versus 29.5% for the S&P 500 That's an annualized return of 27.9% for us and 2.9% for the S&P 500. Once again, a more appropriate index for us is a small or micro cap index, but we beat them by almost the same margins.

Thru December 31, 2010 it was obvious that the work we did rewarded us and our subscribers handsomely.

In spite of our phenomenal returns, I generally do NOT encourage anyone, especially beginners, to subscribe to our service because at least 50% of our subscribers fail to duplicate our published returns.

I do not encourage beginners because they generally lack discipline and they can't tolerate losses.

Peter Lynch, the legendary manager of the Fidelity Magellan Fund, said this a long time ago:

Stock Markets sometimes decline.

If you do not understand that is going to happen, then you will not do well in the stock market.

However, IF you have the discipline and IF you have the intestinal fortitude to follow our advice, THEN you may do well.

Recommendation

If you do NOT have discipline, and if you do NOT have intestinal

fortitude, then you should NOT buy stock OR stock funds because you

will NOT do well.

Full

Disclosure

Past performance is NOT an indicator of future performance. If it

were, then investing would be easy and everyone would be rich, and

that is clearly not possible.

To be continued ...

Notes

Many of my sources for Weather Forecasting statistics and Economic

statistics were found in William A. Sherden's

The Fortune Sellers.

It was a good read.